Currently, BNPL (Buy Now Pay Later), this system has become very popular in the world of digital finance and e-commerce. And it is expected to remain popular in the future. Using this system, you can buy anything. But instead of paying the entire amount at once, you can pay in instalments. Many times, these instalments can be paid without interest.

The BNPL system is so popular that many they use the BNPL system to buy everything from the market. However, this system is much easier, faster, and digital. However, while this BNPL (Buy Now Pay Later) system has its advantages, it also has some disadvantages or risks that you need to know before using it.

Let’s read this article to find out what BNPL is, how it works, and what its advantages and disadvantages.

What is BNPL (Buy Now Pay Later)?

BNPL (Buy Now Pay Later) is a short-term loan scheme. When you buy something from the market, you can pay the money gradually through instalments without paying the full price of the item. However, sometimes if you do not pay the instalment on time, you may be charged a late fee or fine.

Popular BNPL providers include:

-

Klarna

-

Afterpay

-

Affirm

-

Amazon Pay Later

-

LazyPay

-

Simpl

-

ZestMoney

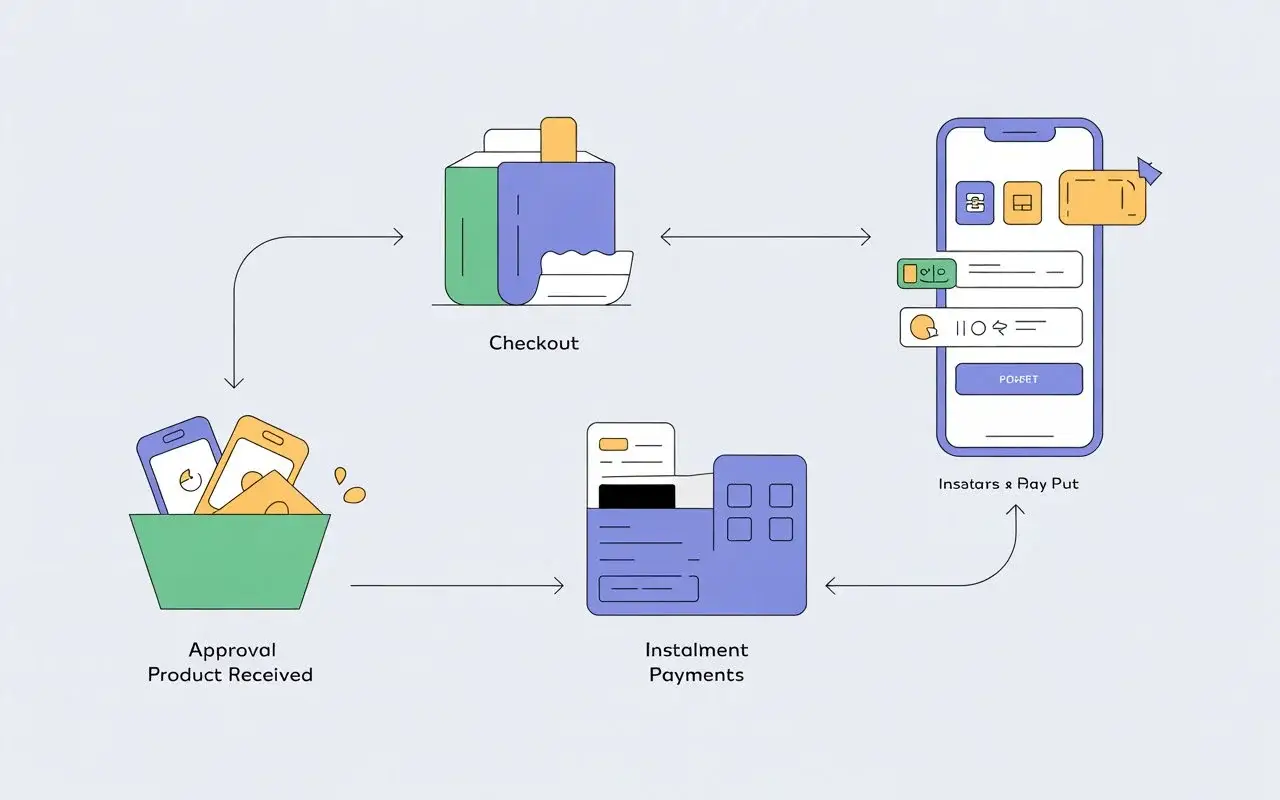

How Does BNPL Work?

The process is quite simple:

-

Select BNPL option – At checkout (online or offline), choose “Buy Now Pay Later.”

-

Verification – The BNPL provider runs a quick KYC or soft credit check.

-

Instant approval – If approved, your purchase is completed instantly.

-

Pay later in instalments – You repay the total amount over a fixed schedule (like 3, 6, or 12 months).

If you buy a phone worth 12,000 through the BNPL system, you will have to pay 3,000 per month for 4 months, or if you want, you can pay in 6 months instead of 4 months.

Advantages of BNPL

1. Instant and Easy Credit

You can get instant credit from BNPL without any complicated process like a loan or a credit card. You don’t have to do heavy paperwork or any other major process for it.

2. Zero or Low Interest Rates

Many BNPL platforms allow you to make payments at zero per cent interest or low interest, if you pay the money on time.

3. Budget-Friendly Purchases

This convenience means you don’t have to pay for large items all at once, which keeps your expenses under control and makes everything easier to shop for.

4. No Credit Card Required

Even those who do not have a credit card can take advantage of this BNPL (Buy Now Pay Later). You just need to have a valid mobile number and a debit card.

5. Fast Digital Process

From signing up to tracking your payments, you can do everything online from your smartphone. You can check your instalment dates and payments all from your phone.

6. Improves Purchase Power

Through this system, you can increase your purchasing power. You can buy things whenever you want, and you can buy your essentials when there is an offer.

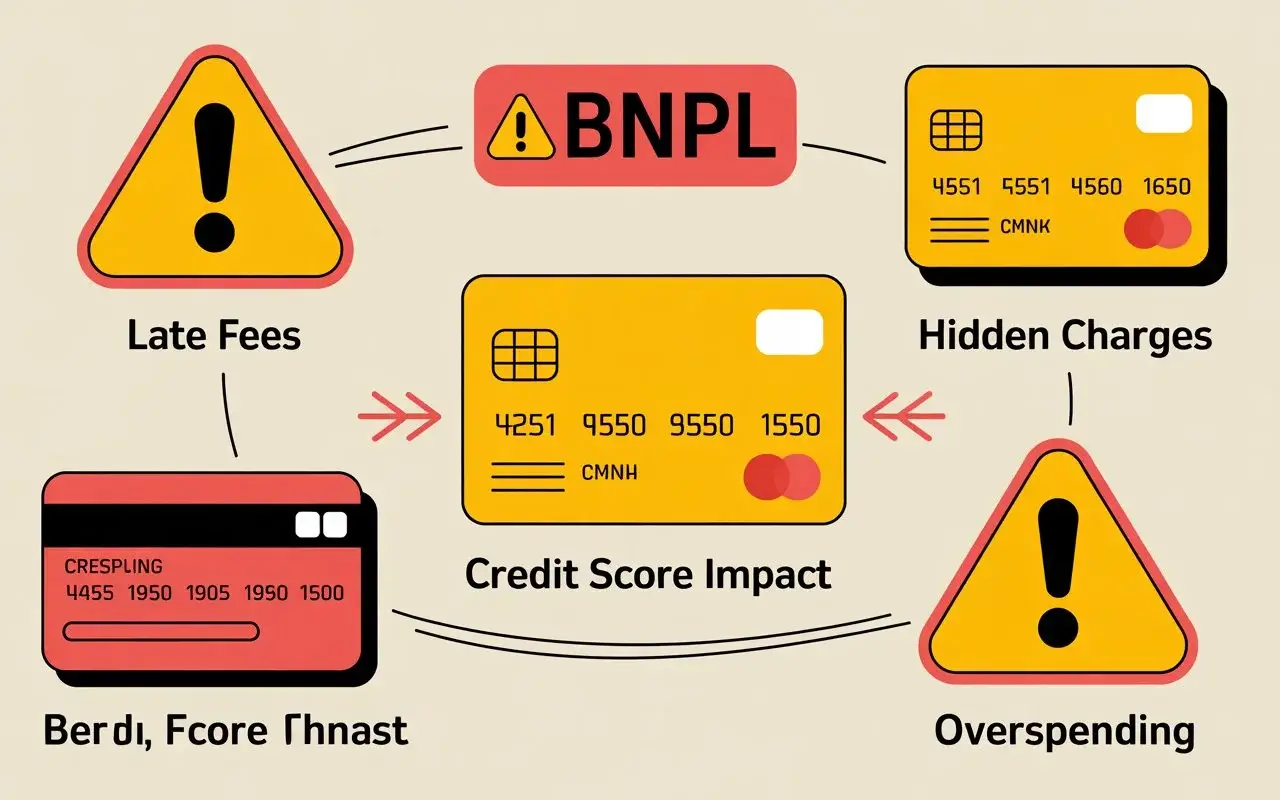

As much as BNPL (Buy Now Pay Later) provides you with benefits, it can also cause you difficulties if you do not use it correctly or consciously.

1. Late Payment Fees

If you don’t make your instalment payments on time, many BNPL companies add late fees and additional charges to your bill.

2. Hidden Charges

There are several platforms that have processing fees or service charges. Many times, users don’t notice them.

3. Encourages Overspending

As a result of this system, since the full amount does not have to be paid immediately, many people end up buying a lot of unnecessary things at once, which later creates a debt burden.

4. Credit Score Impact

If you don’t make your payments on time or if you miss an instalment, your credit rating may deteriorate.

Some suggestions for using BNPL

Here are some tips before using BNPL (Buy Now Pay Later). If you follow them, you won’t have any problems.

- Read all terms carefully: Before purchasing anything, read all the terms and conditions carefully. Check everything first, including when you have to pay, whether there is interest, and whether there are any hidden charges.

- Avoid unnecessary purchases: Buy only what you absolutely need from BNPL; otherwise, don’t use the BNPL (Buy Now Pay Later) system for unnecessary things.

- Track your payments: You need to remember the instalment date after the purchase, and if you want, you can turn on auto pay so that the money is paid on time.

- Use only one or two BNPL apps: Don’t use too many apps, as this will complicate your tracking and make it difficult to remember instalment dates.

- Pay on time: If you pay your instalments on time, your credit score will be good, and you will also avoid penalties.

Is BNPL (Buy Now Pay Later) Safe?

Yes, use trusted platforms to use BNPL, such as Amazon Pay Later, Lazypay, or Simpi.

Before using any app, make sure that the app is approved by the RBI and uses a secure payment gateway. Use all those apps.

Remember, do not disclose or share your OTP or personal information with anyone, and then you can use BNPL safely.

The Future of BNPL in India

In India, BNPL (Buy Now Pay Later) is currently spreading very rapidly in our market, especially among the younger generation and online shoppers. This system has become very popular. Research has shown that India’s BNPL transactions could reach $15 billion and more by 2026.

Various banks and fintech companies are now integrating the BNPL (Buy Now Pay Later) system with credit cards, UPI, and wallets so that more people can take advantage of it. Due to the tightening of RBI regulations, BNPL users will be much safer and more transparent in the future.

Conclusion

BNPL is currently changing the way we shop and spend money, making it easier and faster for everyone to use this system. And in many cases, it has become a great financial asset for the modern generation, as it is interest-free.

However, before using it, you need to be very aware, stay away from unnecessary purchases, avoid late payments, and know the terms and conditions before buying anything. Otherwise, your debt may increase.

FAQs About BNPL(Buy Now Pay Later)

What is BNPL (Buy Now Pay Later)?

BNPL, or Buy Now Pay Later, is a short-term credit option that allows customers to purchase goods or services immediately and pay for them later in installments — often with zero or low interest.

How does BNPL work?

BNPL lets you split your total purchase amount into smaller payments. At checkout, you choose a BNPL provider, complete a quick verification, and repay the amount in fixed instalments over weeks or months.

Is BNPL safe to use?

Yes, BNPL is safe when used through authorised and RBI-regulated providers like Amazon Pay Later, LazyPay, or Simpl. Always read the terms, avoid sharing OTPs, and make timely payments to stay secure.

What are the risks of using BNPL?

If payments are missed, users may face late fees, hidden charges, or even a negative impact on their credit score. Overusing BNPL can also lead to overspending and financial stress.

Which are the top BNPL companies in India?

Popular BNPL companies in India include Amazon Pay Later, LazyPay, Simpl, ZestMoney, and Paytm Postpaid. These platforms offer easy digital credit and flexible repayment plans.